The implementation doesn't hit kudir. Correct reflection of expenses in kudir

It happens that there are situations when, when entering all the documents, the expected expenses are not displayed in the book of expenses and income.

Let's consider the most common reasons why expenses reflected in accounting are not displayed in KUDIR.

1. Props "Expenses (NU)"

In accordance with Art. 346.16 of the Tax Code of the Russian Federation, the list of accepted expenses is closed, i.e. only those expenses that are explicitly listed in this article can be taken into account in the composition of expenses.

During the reflection of expenses in the program, it is indicated whether these expenses are accepted or not, that is, they comply with the requirements of Art. 346.16 of the Tax Code of the Russian Federation or not.

For example, in the document "Receipt of goods and services", reflecting the services of a third-party organization, it will look like this.

Fig.1 "Document - Receipt of goods and services"

It is worth noting that expenses are considered not accepted if the requisite “Expenses (NU)” is not filled in.

As for goods and materials, there are certain difficulties. For them, the acceptability of expenses is determined by both receipt and write-off.

For example, despite the fact that in the receipt document, for materials and goods it is indicated “accepted”, expenses for nm will not be accepted if, for example, the materials were written off for non-acceptable expenses, and the goods were sold for taxable UTII activities.

Another example is the gratuitous receipt of materials. Such materials will not be accepted as expenses. Even if the requirement - invoice indicate "accepted", in the receipt document in the column "Expenses (NU)" it will be indicated "not accepted".

2. Payment and other necessary conditions

In accordance with the requirement of the cash basis, expenses will be recognized only after actual payment.

For certain types of expenses, there are additional conditions, for example, expenses for the purchase of goods cannot be accepted before they are sold.

The program performs automatic control of all necessary conditions, and until all necessary events are reflected, the flow rate will not be displayed in KUDIR. Therefore, the second reason may be the fact that the expenses were not paid or certain events did not occur that are necessary for the recognition of the expense.

3. The sequence of documents

One of the most common reasons is backdating of documents.

When working with documents backdated, you must retransmit all later documents related to these costs. If you cannot establish a connection, you will have to rewire everything.

4. Initial balances

In the simplified taxation system, in special accrual registers, special accounting is maintained. These registers contain information about consignments of goods and materials, mutual settlements, and specific information about expenses.

Initial balances must be entered into these registers, that is, if there are expenses associated with transactions made before the start of accounting or before the transition to a simplified taxation system, then this information must be entered. If you do not enter the initial balances, then the expenses may not fall into KUDIR, here is another reason.

5. Date of accounting relevance

In "1C: Accounting 8" there is a mechanism that allows you to speed up the work of splitting the document into two stages - quick registration of the document and final posting in batch mode. In this mechanism, there is such a thing as the date of relevance of accounting - before this date, the accounting is relevant and the documents have been completed in full, and after this date, the documents are still waiting for final completion. In view of this, expenses may not be recognized if the document is not fully posted (located later than the date of relevance).

6. Mutual settlements on settlement documents only for tax accounting

This situation is quite rare, but since it is difficult to identify it on your own, it deserves a separate description.

In 1C: Accounting 8, accounting for mutual settlements under an agreement with a counterparty can be done in two ways:

- under the contract as a whole;

- According to billing documents.

Accounting for mutual settlements for the purposes of the simplified tax system also works. It is possible that in the settings of accounting parameters, the maintenance of the "Settlement document with counterparty" analytics is disabled, but agreements "on settlement documents" are used. In this case, according to accounting, it is not noticeable that advances and payments are not closed, and in tax accounting, expenses are considered unpaid and are not reflected in KUDIR.

In such a situation, it is recommended that the documents correctly fill in the details “settlement document” or refuse to use agreements with mutual settlements “according to

settlement documents” and use an agreement with mutual settlements under the “contract as a whole” instead.

Analysis of the state of expenses to be reflected in tax accounting under the simplified tax system

The accumulation register "Expenses under the simplified tax system" stores information about each expense of the organization, which can be reflected in the KUDIR.

The most interesting information is:

- for what reasons, and what expenses are not accepted for tax accounting;

- What needs to be done in order for these expenses to be accepted for tax accounting.

Expense statuses can take the following values:

- Not written off;

- Not written off, not paid;

- Not paid;

- Not paid, not paid by the buyer;

- Not paid by the buyer.

In the report, set the following settings (Figure 2-3).

USN: recognition of income and expenses (1C Accounting 8.3, edition 3.0)

2016-12-08T11:39:01+00:00Today we will analyze the topic that causes, perhaps, the largest number of questions from novice (and not only) accountants - the procedure for recognizing income and expenses under the simplified taxation system (STS) in the 1C: Accounting 8 family of programs.

Examples will be considered in 1C: Accounting 8.3 (edition 3.0). But in the "two" everything works the same way.

A short digression into the theory

We are interested in filling out the book of income and expenses (KUDIR). In this wonderful book:

- column 4 is the column "Total income"

- column 5 is "Accepted income"

- column 6 is the column "Total expenses"

- column 7 is "Expenses Accepted"

We are primarily interested in columns 5 and 7. It is they that affect the amount of the single tax we pay.

There are two main modes on the "simplified":

- income (column 5)

- income (column 5) minus expenses (column 7)

To calculate a single tax in the first case, we simply multiply the amount of income by 6%, and in the second case we multiply the difference between income and expenses by 15%.

In short, that's all.

Correctly calculate income and expenses - this is the most difficult task. Based on the very presence of four columns "total income" and "received income", "total expenses" and "received expenses" it turns out that not all income and expenses can be taken for tax calculation.

You need to be able to correctly determine the moment of recognition of income or expense. With the simplified tax system, for this it is mandatory to use cash basis.

Under the cash method, the date of receipt of income is the day when funds are received in bank accounts or at the cash desk. And it doesn't matter if it's an advance payment or a payment. The money came - the income was received, and therefore immediately falls into columns 4 and 5.

As you can see, with income, everything is extremely simple. Any receipt of money (to the cashier or to a current account) falls into the general and recognized income, from which tax must be paid.

With expenses, things are a bit more complicated.

For recognition expenses for the purchase of materials- it is necessary to reflect the fact of their receipt and payment.

For recognition expenses for services rendered to us- it is necessary to reflect the fact of their provision and payment.

For recognition expenses for the purchase of goods for subsequent resale - you need to reflect the fact of their receipt, payment and sale.

For recognition labor costs- you need to reflect the fact of its accrual and payment.

When paying through expense reports- in addition to the above conditions, it is required to reflect the fact of issuing money to an accountable person.

As you can see, for many of these situations, there are several conditions for recognizing an expense at once. And these conditions can be met in a different order. In this case, the moment of recognition of the expense will be considered last condition met.

Bank advance from buyer

The buyer transferred the money to our current account as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into "Total income" (column 4) and "Income taken into account" (column 5):

bank receipt -> column 4 + column 5

We issue an extract (receipt to the current account) for 2000 rubles from the buyer LLC "Magic Doe":

We conduct and open document postings (DtKt button). We see that the amount of payment was related to 62.02 - that's right, because this is an advance:

Immediately go to the second tab "Book of accounting for income and expenses." It is here that the payment amounts are posted (or not posted) according to the KUDIR columns. We see that the received 2000 rubles fell immediately into columns 4 and 5:

Advance payment from the buyer at the checkout

With a cash register, everything is similar to a bank. The buyer paid money to the cashier as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into columns 4 and 5:

receipt at the checkout -> column 4 + column 5

We issue an incoming cash order (cash receipt) from the buyer "Svergunenko M.F." for the amount of 3000 rubles:

We post the document and proceed to its postings (button DtKt). We see that the amount of payment was related to 62.02 - that's right, because this is an advance:

We immediately go to the tab "Book of accounting for income and expenses" and see that our total amount fell into columns 4 and 5:

Paying a provider for services rendered

Let's move on to expenses. Everything is more interesting here. But not in the case of payment for services rendered to us. It is enough for us to enter into the program an act on the provision of services and its payment, then the act itself (according to the cash method) will not make any marks in the columns KUDIR, but the bank statement will immediately spread the amount of payment in columns 6 and 7:

service act -> will do nothing

bank payment -> column 6 + column 7

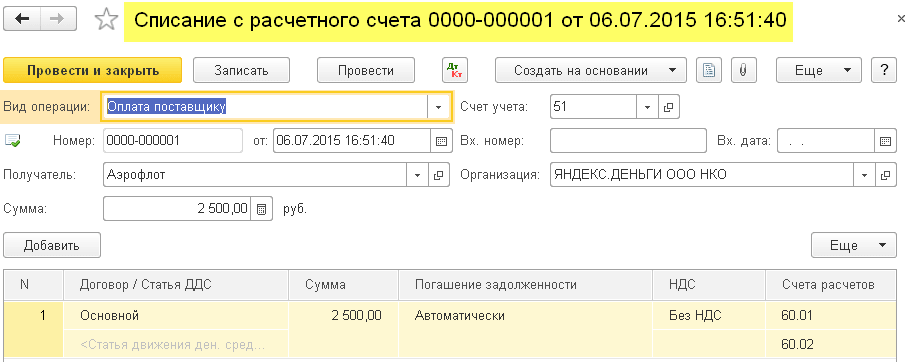

We enter into the program an act on the provision of services from the supplier "Aeroflot" in the amount of 2500:

We post the document and proceed to its postings (button DtKt). We see that the costs (account 26) were attributed to 60.01 - that's right:

We do not see the bookmarks "Book of income and expenses", which means that the indicated 2500 did not fall into any of the KUDIR columns. Go ahead.

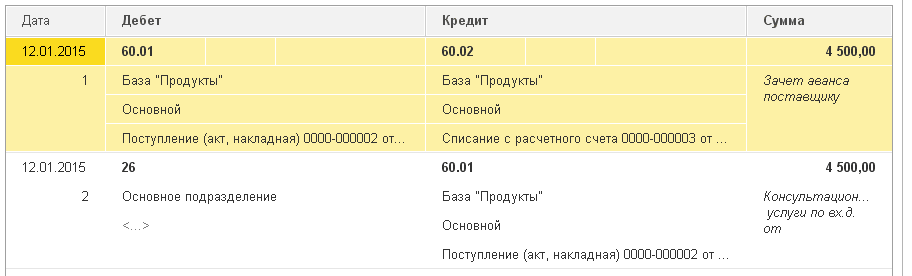

On the following day, we submit an extract on payment for the services rendered to us:

We carry out an extract and look at its postings. We see that the amount of payment is related to 60.01:

We immediately go to the "Book of income and expenses" tab and see that the paid 2500 finally fell into columns 6 and 7:

Advance payment to the supplier for the provision of services

What if we made an advance payment to the supplier for the services rendered (advance payment)? And then they issued an act on the provision of services. Schematically it will look like this:

bank payment -> fill in column 6

act on the provision of services -> fill in box 7

We will add a bank statement to the program (our advance payment to the supplier) in the amount of 4500:

Let's post the document and open its postings (button DtKt). We see that the amount hit 60.02 - that's right, because this is an advance:

Immediately go to the tab "Book of income and expenses" and see that the amount of the advance fell only in column 6:

And it is right. According to the cash method in column 7 (expenses accepted), we will be able to take this amount only after the submission of the service act. Let's do it.

We will add an act on the provision of services to the program the next day:

Let's go through the document and see the postings:

Let's immediately go to the "Book of income and expenses" tab and see that the amount of payment finally got into the seventh column:

Paying the supplier for materials

Important!

Next, we will argue like this. We have a cash method. First, there was the receipt of materials, then payment by bank. Obviously, it is the payment by the bank (since the receipt has already been) that will create entries in columns 6 and 7. Schematically, it will be like this:

material receipt -> will not create anything

bank payment for materials -> fill in column 6 and column 7

We will include in the program the receipt of materials in the amount of 1000 rubles:

We see that next to the postings, the tab "Book of income and expenses" did not appear. This means that the goods receipt document in this case did not create records for any of the KUDIR columns.

We will issue a statement of payment for materials on the following day:

Let's post the document and open its postings (button DtKt):

Let's immediately go to the tab "Book of income and expenses" and see that the document filled out columns 6 and 7:

Advance payment to the supplier against the supply of materials

Important! First, we will correctly set up the procedure for recognizing expenses in the accounting policy -.

In this case, first comes the payment, then the receipt of materials. According to the logic of the cash method, full recognition of expenses (column 7) will be possible only after the execution of both documents. Schematically it will be like this:

payment by bank against the supply of materials -> fill in column 6

receipt of materials -> fill in column 7

We will add to the program an extract on prepayment for materials for 3200 rubles:

Let's post the document and open its postings (button DtKt):

Let's immediately go to the tab "Book of accounting for income and expenses" and we will see that the extract has filled in only column 6 so far (total expenses):

To fill in the seventh column, the document receipt of materials is missing. Let's format it:

We post the document and look at its postings (button DtKt):

Immediately go to the tab "Book of accounting for income and expenses" and see that the document receipt of materials filled in the missing column 7:

Payment to the supplier for goods

Important! First, we will correctly set up the procedure for recognizing expenses in the accounting policy -.

In general, the procedure for recognizing expenses for the purchase of goods for sale is similar to the situation with the receipt of materials - it also requires receipt and payment. But an additional (third) requirement is that Expenses are recognized only as the purchased goods are sold..

Schematically, our scheme will be as follows:

receipt of goods -> fills nothing

payment for goods by bank -> fill in column 6

sale of paid goods -> fill in column 7

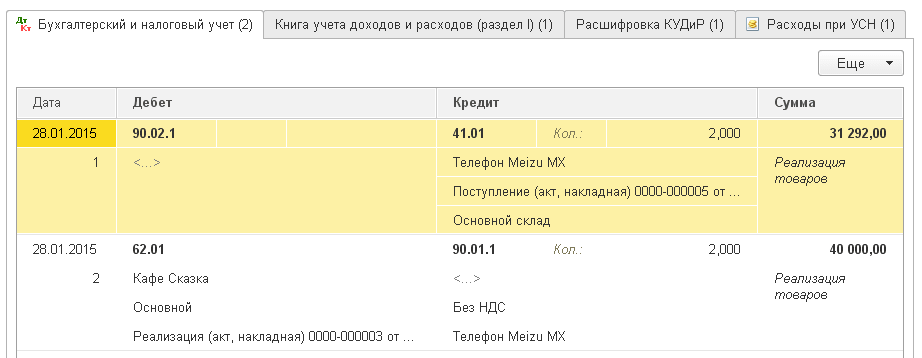

We will include in the program the receipt of goods in the amount of 31292 rubles:

Let's post the document and open its postings (button DtKt):

We see that the tab "Book of accounting for income and expenses" is missing, which means that the document did not record anything in the KUDIR columns.

We will make a statement of payment for goods to the supplier:

Let's check the document and open its postings:

Immediately go to the tab "Book of accounting for income and expenses" and see that the amount of payment fell into the total expenses (column 6). In the seventh column (expenses accepted), this amount will fall as the goods are sold.

Let's assume that all goods are sold. Let's implement it:

Let's post the document and open its postings (button DtKt):

Let's immediately go to the tab "Book of accounting for income and expenses" and we will see that the amount of payment finally fell into the seventh column:

Advance payment to the supplier for goods

Important! First, we will correctly set up the procedure for recognizing expenses in the accounting policy -.

Everything here is similar to paying the supplier for goods (previous paragraph). Except that the amount of payment will fall into the sixth column of the first document (bank statement). The schema will be like this:

payment for goods by bank -> fill in column 6

receipt of goods -> will not fill anything

sale of paid goods -> fill in column 7

Payment to the supplier through the advance report

Important! First, we will correctly set up the procedure for recognizing expenses in the accounting policy -.

If, in any of the situations described above, you replace payment through a bank with payment through an accountable person, everything will work in exactly the same way.

But there is a nuance. The main condition for taking the expenses paid according to the advance report (in addition to those listed above) is the actual issuance of money to the accountable person (cash order).

It is the RKO document that column 6 will be filled in.

Column 7 will be filled in upon the occurrence of the following additional conditions: advance report + (certificate of service provision or receipt of material or receipt of goods and its sale). Moreover, this column will be filled with the latest document by date.

Payment of wages

To fill in columns 6 and 7, you must have two documents at once: accrual and payment of salaries.

Scheme 1:

payroll -> will not fill anything

payroll (RKO) -> fill in column 6 and column 7

Scheme 2:

payment of wages before accrual (CSC) -> fill in column 6

payroll -> fill in column 7

We are great, that's all

By the way, new lessons...

Sincerely, Vladimir Milkin(teacher and developer

All taxpayers using the simplified taxation system (STS) are required to keep a book of income and expenses (KUDiR). If you do not do this, or fill it out incorrectly, you can get a considerable fine (Article 120 of the Tax Code of the Russian Federation). This book is printed and handed over to the tax office at their request. It must be stitched and numbered.

Before you start creating this book of income and expenses in 1C 8.3, check the program settings. If you have problems with the formation of KUDiR and some expenses do not fall into the book, carefully double-check the settings. Most of the problems lie here.

Where is the book of income and expenses 1C 8.3? In the "Main" menu, select the "Settings" section item.

You will see a list of configured accounting policies by organization. Open the position you need.

In the form of setting up an accounting policy at the very bottom, click on the hyperlink "Setting up taxes and reports".

In our example, the “Simplified (income minus expenses)” taxation system is selected.

Now you can go to the "STS" section of this setting and set up the procedure for recognizing income. It is here that it is indicated which transactions reduce the tax base. If you have a question why the expense does not fall into the book of expenses and incomes in 1C, first of all, look at these settings.

Some items cannot be unflagged as they are mandatory. Other flags can be set based on the specifics of your organization.

After setting up the accounting policy, let's move on to setting up the printing of KUDiR itself. To do this, in the "Reports" menu, select the item "Book of income and expenses of the STS" of the "STS" section.

You will see the ledger report form. Click on the "Show Settings" button.

If you need to detail the records of the received report, check the corresponding flag. The rest of the settings are better to check with your tax office, having learned the requirements for the appearance of KUDiR. In different inspections, these requirements may differ.

Filling in KUDiR in 1C: Accounting 3.0

In addition to the correct settings, before the formation of KUDiR, it is necessary to complete all operations for closing the month and check the correct sequence of documents. All expenses are included in this report after they are paid.

The R&D accounting book is generated automatically and quarterly. To do this, click on the "Generate" button in the form where we just made the settings.

The book of income and expenses contains 4 sections:

- Section I This section reflects all income and expenses for the reporting period on a quarterly basis, taking into account the chronological sequence.

- ChapterII. This section is filled out only with the form of the simplified tax system "Income minus expenses". It contains all the costs of fixed assets and intangible assets.

- ChapterIII. It contains losses that reduce the tax base.

- ChapterIV. This section displays amounts that reduce tax, for example, insurance premiums for employees, etc.

If you configured everything correctly, then KUDiR will be formed correctly.

Manual adjustment

If, nevertheless, KUDiR was not filled in quite the way you wanted, its entries can be corrected manually. To do this, in the “Operations” menu, select the item “Entries in the book of income and expenses of the simplified tax system”.

In the opened list form, create a new document. In the header of the new document, fill in the organization (if there are several of them in the program).

This document has three tabs. The first tab corrects entries in section I. The second and third tabs correct entries in section II.

If necessary, make the necessary entries in this document. After that, KUDiR will be formed taking into account these data.

Analysis of the state of accounting

This report can help you visually check the correctness of filling out the book of income and expenses. To open it, select the item "Accounting analysis according to the simplified tax system" in the "Reports" menu.

If the program keeps records for several organizations, you need to select the one for which the report is required in the report header. Also set the period and click on the "Generate" button.

The report is divided into blocks. You can click on each of them to get a breakdown of the amount.

Colleagues!

Often in our practice there are questions about the acceptance of expenses in KUDiR.

It seems that they did everything: they received and entered the invoice into the database, paid the invoice to the supplier, shipped the goods to the buyer, and the costs are not recorded in KUDiR.

And what to do?

You have to enter these expenses with the document Entries in the Book of Income and Expenses.

But this means doing double work and, possibly, getting an error in the future.

So, let's try to answer the question "why" this happens and how to check the conditions for accepting costs as expenses.

So let's start...

Preliminary remarks: consider the accounting policy settings:

- Accounting policy - tab STS - Procedure for recognition in expenses:

It all depends on the settings of the accounting policy.

We carefully analyze the noted data: in order of recognition of expenses, it is worth

Receipt of goods, payment for goods and sale of goods. Those. if you have a tick "Sale of goods", then paying for the goods and posting the goods for recognition of expenses in KUDiR will not be enough for you. Then, the costs will fall into the expenses of KUDiR only after the shipment of the goods. And if there is a tick "Receiving income (payment from the buyer)", then receiving payment from the buyer.

This is the most important thing to always start with.

2. The second very important point: checks on cost accounting in NU.

This will have to be done by checking the documents of the vocational school, the requirements for invoices, etc., where there is a record of NU Expenses. You may have selected the wrong cost item ( not taking into account expenses at NU).

3. If everything according to paragraphs. 1-2 You have checked, then work begins with the accumulation register Expenses under the simplified tax system.

Build a report on it in the Universal Report with a selection by an expense element that is not taken into account in the KUDIR and analyze the received data.

According to the register “Expenses under the simplified tax system”, it is possible to determine which expenses have not yet been accepted for tax accounting, for what reasons, what must happen in order for a specific expense to be accepted for tax accounting.

The general scheme for accepting expenses:

— Receipt of goods (PTU): Not written off, not paid

— Payment to the supplier (Statement): Not written off

— Implementation (RTU): Not paid by the buyer

— Payment from the buyer (Statement): Accepted as expenses.

Depending on what you have in your accounting policy, the last two conditions may or may not be taken into account when taking into account.

In our case, the “Not paid” status shows that you have not paid for the vocational school to the supplier, therefore you cannot accept the amounts as expenses

And the Status is “not written off” - there is no sale of the purchased goods, therefore, again, it cannot be taken into account.

Status "not written off, not paid" - the goods have not been paid to the supplier and there is no sale for it.

Here is an example of compiling a report on the accumulation register Expenses under the simplified tax system:

Accountants whose organizations are on the simplified tax system periodically complain that KUDiR in 1C Accounting 3.0 is filled out incorrectly. It happens that entries from the balance sheet do not end up in the income and expense book as expected. The publication will consider the most common errors that occur when maintaining a simplified taxation system in 1C Accounting 3.0 and propose 1C processing to correct accounting errors.

In order to connect the terminology of accountants and programmers for communication in a common language, I will make a few clarifications:

- The object of the 1C platform "Register of accounting" stores accounting entries, the main report using accounting entries is the "Turnover balance sheet". Therefore, the terms accounting register data" and " balance sheet data” represent one essence.

- KUDiR- short for " Income and expense ledger“, which is conducted by organizations and entrepreneurs with a simplified taxation system for calculating the tax base. According to the Book, taxes are paid in accordance with the tariff: 6% of the tax base (Only income) or 15% of the tax base (Income - Expenses).

For an unambiguous understanding of the problem, let's look at the causes of USN errors in 1C Accounting 3.0.

The main reasons for the occurrence of errors in accounting for the simplified tax system in 1C Accounting 3.0

In fact, there are not many reasons, and all of them are related to a misunderstanding of the operation of the 1C cost accounting mechanism. Comrade users, the entries in the income and expense ledger are not formed according to the data of the accounting register (balance sheet), but according to data from completely different registers.

So I want to write in bold letters again that

the amounts falling into KUDiR are not taken from the accounting register or the balance sheet, but are formed in separate registers 1C Accounting 3.0

All these registers will be discussed below. And I pay so much attention to this issue because

when maintaining the simplified tax system in 1C Accounting 3.0, introducing a manual operation with adjustments accounting register only(amounts in the balance sheet) without adjusting the registers of the simplified tax system, you 100% make a mistake!!!

After entering a manual transaction, the data becomes correct in the balance sheet, but the expense offsets are not correct! Therefore, if you want to correct something in salaries, taxes, goods, consult people who know how to do it correctly in 1C Accounting 3.0. By doing this, you will ultimately win in saving your time and nerves in the future, when submitting reports.

The problem is further aggravated by the fact that accounting periods are closed after the reporting period, and correcting errors in the closed period can lead to discrepancies between the submitted reports and 1C data. Therefore, when KUDiR in 1C Accounting 3.0 is filled in incorrectly, then the only correct decision is to correct the data at the beginning of the open period and do a general re-posting of documents, as a result of which a correct book of income and expenses should be formed.

How to do it yourself, I will show you below in this article. And now we will consider the accounting policy settings for the simplified tax system, since sometimes KUDiR in 1C Accounting 3.0 is filled in incorrectly due to incorrect accounting policy settings.

Setting up an accounting policy for the simplified tax system in 1C Accounting 3.0

The accounting policy settings for the simplified tax system are set before the start of accounting and, in theory, do not change during the year.

In order to correctly change the accounting policy for the simplified tax system in the middle of the year, it is necessary to retransmit all documents from the beginning of the year after the change.

To study the method of correcting accounting under the simplified tax system, when KUDiR in 1C Accounting 3.0 is filled out incorrectly, we will create a new organization in the Organization directory - IP - with a simplified taxation system of 15%. In the card, fill in the basic details manually or by TIN if the 1C Counterparty service is connected. After filling, we proceed to setting up the taxation system, indicating that the organization has a taxation system Simplified (income minus expenses).

The most important settings for the simplified taxation system in 1C Accounting 3.0 are on the second tab "STS".

In this tab, for each type of STS expense, you can set the recognition procedure. Checkboxes, without the possibility of withdrawal, indicate the events of recognition of expenses, fixed by law. Whether or not to consider events with the possibility of change when recognizing expenses, each organization decides independently by checking or unchecking the appropriate boxes. So,

in the absence of expenses in KUDiR, when the necessary conditions for recognizing expenses are met, see in the settings for the recognition of expenses of the simplified tax system for additional expense recognition events.

Correction of errors in the recognition of expenses for goods and materials

Let us consider the mechanism of formation of expenses for KUDiR for purchased goods and materials. For a better understanding of the actions to correct the accounting of the simplified tax system, we will create the simplest accounting situation.

First of all, we will deposit a founder's contribution to the authorized capital of 10,000 rubles to the bank account.

We make payment for goods and materials, for this we transfer an advance payment to the supplier in the amount of 4720 rubles (including 720 rubles VAT). In this case, the posting Dt 60.02 Kt 51 will be generated and the entire amount of payment falls into column 6 “Total expenses” of KUDiR.

We make the arrival of paid stock items, and we break the receipt into goods in the amount of 3 units. and come to account 41.01 for resale and materials in the amount of 1 unit. on account 10.01. to use for your own purposes. 1C Accounting will generate receipt postings, but only payment for the purchased material will be included in the book of income and expenses.

The received items of goods did not fall into the KUDiR, since the settings for the USN indicate that events are necessary for the recognition of expenses on purchased goods: the purchase of goods, their payment and sale. For the recognition of materials as expenses, a sufficient condition is the purchase of materials and their payment:

Accordingly, the goods will go to KUDiR after the sale. We will make the sale of one unit of products out of the three purchased, in order to check the operation of the mechanism for recognizing expenses under the simplified tax system. We draw up a document for the sale of purchased products (by the way, if you need to display gross records in TORG 12, then we read the publication Gross in TORG 12 for 1C Accounting 3.0).

Indeed, after registration of the sale, we see the records of the consumption of one commodity unit in the records of the book of income and expenses of the simplified tax system.

The example shows how the initial settings of the system affect the formation of entries in the ledger of income and expenses of the simplified tax system. So,

if you have not generated records in KUDIR, then look at the settings for the events of recognition of expenses of the simplified tax system and check the entire path of the movement of goods or material - from purchase to sale or consumption in the organization.

This rule will apply if the entries do not end up in the Book at all after the completed events. But more often there are situations when the recognition of expenses occurs incorrectly.

Finding and correcting errors when KUDiR in 1C Accounting 3.0 is filled out incorrectly

One example of such an error is when you sell goods for one amount, and another amount enters the KUDiR. In this case, the 1C programmer is called and they begin to prove with great predilection that the program does not work correctly !!! 😡

A little more knowledge is needed to correct these kinds of errors. If you pay attention to the registers for which 1C Accounting 3.0 makes postings, then when conducting trading operations notice the movements in the register Expenditures under USN. This register accumulates all expenses that should fall into the KUDiR of the simplified taxation system. Accordingly, this register must be looked at when for trading operations KUDiR in 1C Accounting 3.0 is filled out incorrectly.

You can view the data of the accumulation register “Expenses for the simplified tax system” through the “Universal Report” (located in the “Reports” section), where we select the register and set up groupings and indicators. The accounting register data is formed in the balance sheet. To make a reconciliation, it is necessary to form both of these registers for the same period and examine the data for discrepancies.

If you want to understand the nature of the error, check the turnovers and calculate the operations due to which the accounting has “dispersed”. If you need to make a correction of a previously made mistake, then look at the balances and, in case of discrepancies, make an adjustment to the register “Expenses for the simplified tax system”. Theoretically, you can also edit the accounting register, but usually accountants are guided by the data of the balance sheet, so the data in this report are taken as true.

To enter the adjustment, the Operation document is used, in which the edited register is selected, in our case, “Expenses under the simplified tax system”.

With the help of this document, we bring the balances of the register "Expenses under the simplified tax system" to the balances of the balance sheet. After that, it is necessary to make a general re-posting of documents from the moment of correction, and then the entries in KUDiR will be accepted correctly.

The publication discussed the correction mechanism trading operations, in which KUDiR in 1C Accounting 3.0 is filled out incorrectly. If you noticed, throughout the article it was emphasized that we are talking about trading operations. The fact is that operations on settlements with employees and settlements with funds are formed differently. In the next post, we will talk about this.

See you soon!

KUDiR in 1C Accounting 3.0 is filled out incorrectly, how to fix it (part 1)